The global financial crisis of 2008-2009 highlighted the need for strong regulation in the banking and finance sector. The failure of several large banks and financial institutions demonstrated the potential risks that could arise from poor risk management, lack of transparency, and excessive leverage in the market. In response to this crisis, international regulators came together to design a new set of capital regulations known as Basel III. This set of regulations aims to strengthen the global financial system by increasing the resilience and stability of banks and other financial institutions.

Toc

Introduction to the Capital Regulation Plan

The Capital Regulation Plan (CRP) is an important regulatory framework that governs the financial industry. It sets guidelines for banks and other financial institutions to maintain a certain level of capital in order to ensure their stability and ability to absorb potential losses. This plan was first introduced after the 2008 global financial crisis, in which many banks failed due to inadequate capital reserves.

Understanding Capital Regulation

Capital regulation refers to the rules and guidelines that govern how much capital a bank or financial institution is required to hold in order to mitigate potential risks. In simple terms, capital is the amount of money a bank has available to absorb losses before it becomes insolvent. The higher the level of capital a bank holds, the more cushion it has in case of unexpected losses.

The primary purpose of capital regulation is to ensure that banks and other financial institutions maintain a healthy level of financial stability. This is important because if a bank fails, it can have severe consequences on the overall economy and cause a ripple effect across various sectors.

Definition and Significance

Capital regulation refers to the set of standards and requirements that dictate the minimum amount of capital financial institutions must hold in relation to their assets. These regulations are integral to mitigating risks and ensuring that banks can withstand financial distress without collapsing.

Basel III: The New Global Standard

Basel III is the third set of international banking regulations developed by the Basel Committee on Banking Supervision (BCBS). It was first introduced in 2010 as a response to the global financial crisis and has since been implemented by over 100 countries.

The main objective of Basel III is to enhance the resilience and stability of banks by increasing their levels of capital, liquidity, and risk management. It also aims to improve the transparency and consistency of capital regulations across different countries.

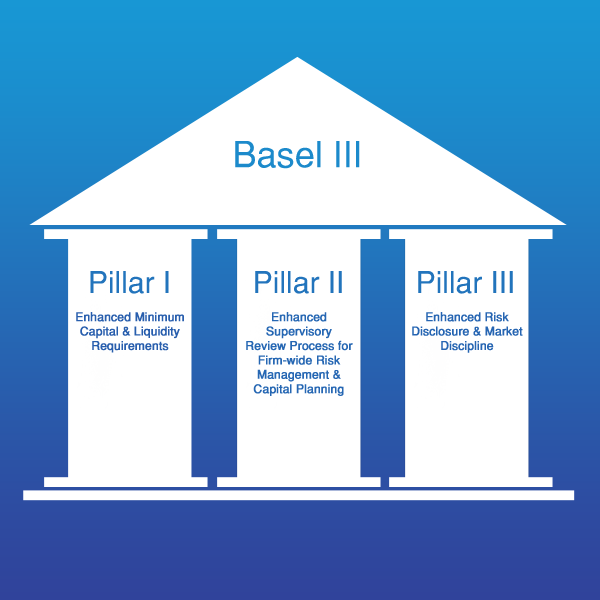

The Three Pillars of Basel III

Basel III is based on three pillars, each addressing a different aspect of bank regulation:

- Minimum capital requirements – This pillar sets out guidelines for banks to maintain a minimum level of capital in relation to their assets and risks.

- Supervisory review process – Under this pillar, regulators are required to conduct regular reviews of banks’ risk management practices and ensure they have adequate capital reserves.

- Market discipline – This pillar promotes transparency and disclosure in the banking industry, allowing market participants to make informed decisions about their investments.

Key Components of the Plan

The specific capital regulation plan under discussion includes stringent capital adequacy requirements, leverage ratios, and liquidity standards. These components are designed to bolster the financial system’s stability and resilience against economic volatility. Let’s take a closer look at each of these components.

Capital Adequacy Requirements

One of the main pillars of the CRP is capital adequacy requirements, which seek to ensure that banks hold enough capital to cover potential losses. This component is based on the concept of risk-weighted assets, where different types of assets are assigned varying levels of risk. Banks are required to maintain a certain ratio between their capital and risk-weighted assets, with higher-risk assets requiring more capital reserves.

Leverage Ratios

Leverage ratios measure a bank’s level of debt relative to its capital. A high leverage ratio means that a bank has borrowed more money than it can handle, making it more vulnerable to financial distress. Under the CRP, banks are required to maintain a leverage ratio of 3%, meaning that their total assets should not exceed 33 times their capital.

Liquidity Standards

Liquidity refers to a bank’s ability to meet its short-term financial obligations without incurring significant losses. The CRP includes liquidity standards that require banks to hold enough liquid assets (such as cash and government bonds) in case of sudden withdrawals or market disruptions.

Introduction to Capital Requirements

Capital requirements are the minimum amount of funds that banks must hold as a percentage of their assets. These requirements act as a cushion against potential losses and help maintain the stability of financial institutions.

The most common types of capital requirements are:

Tier 1 Capital

Tier 1 capital is a crucial component of a bank’s financial strength and represents the core equity capital that banks must hold. It primarily consists of common equity tier 1 (CET1) capital, which includes common shares, retained earnings, and other comprehensive income. The significance of Tier 1 capital lies in its ability to absorb losses while a bank is going concern, limiting the likelihood of insolvency and ensuring that the bank remains operational during financial stress.

Regulators require banks to maintain a minimum Tier 1 capital ratio, which is the ratio of Tier 1 capital to risk-weighted assets (RWA). This ratio serves as an indicator of a bank’s financial health and its ability to withstand potential losses. Under Basel III, the minimum requirement for the Tier 1 capital ratio is set at 6%, which reflects a substantial increase from previous regulations. By enforcing higher capital requirements, regulators aim to bolster the resilience of banks and protect the broader financial system from shocks, thereby fostering trust and stability within the investment community.

Tier 2 Capital

Tier 2 capital serves as a supplementary layer of financial protection for banks, enhancing their overall capital structure. This tier includes subordinated debt, preference shares, and certain hybrid instruments, which can absorb losses in the event of a bank’s financial distress. While not as secure as Tier 1 capital, Tier 2 capital still plays a vital role in bolstering a bank’s capacity to withstand fluctuations and potential insolvency.

Regulatory frameworks, including Basel III, mandate that banks hold a minimum Tier 2 capital ratio as part of their overall capital requirements. Specifically, under Basel III, the total capital ratio must be at least 8%, comprising a combination of both Tier 1 and Tier 2 capital. This holistic approach to capital requirements ensures that banks have sufficient resources to navigate adverse economic conditions while maintaining confidence among depositors and investors.

The Role of Capital Buffers

In addition to meeting minimum capital requirements, Basel III introduces the concept of capital buffers, which are additional layers of capital that banks must hold during stable economic times. These buffers can be drawn upon in times of stress, enabling banks to absorb losses while continuing operations. The capital conservation buffer, for instance, requires banks to maintain a buffer above the minimum capital requirement to avoid restrictions on capital distributions such as dividends. This proactive measure aims to ensure that banks remain resilient, even during periods of economic turbulence, thereby fostering stability in the financial system as a whole.

The Impact of Capital Regulation on Finance

The implementation of Basel III has had a significant impact on the banking and finance industry. Here are some key ways in which the CRP has shaped finance:

1. Increased Stability and Resilience

The most notable impact of the Capital Regulation Plan, particularly Basel III, is the enhanced stability and resilience of financial institutions. By enforcing stricter minimum capital requirements, banks now hold a larger capital buffer that can absorb unexpected losses. This precautionary measure not only protects individual banks from financial distress but also contributes to the overall stability of the banking system. As a result, in times of economic uncertainty or downturns, banks are better positioned to weather the storm and continue operating, which is crucial for maintaining public confidence in the financial system.

2. Improved Risk Management Practices

The introduction of Basel III has prompted banks to reassess and improve their risk management frameworks. Given the heightened scrutiny from regulators and the necessity to maintain adequate capital reserves, financial institutions have adopted more proactive approaches to identify, quantify, and manage risks. This shift has resulted in more robust stress testing and scenario analysis, allowing banks to understand potential vulnerabilities and mitigate them effectively. By prioritizing comprehensive risk management, banks can make more informed lending and investment decisions, leading to healthier financial portfolios.

3. Greater Market Transparency

Another significant effect of the Capital Regulation Plan is the push for increased transparency in the banking sector. Basel III’s emphasis on market discipline encourages banks to provide more detailed disclosures regarding their financial health, risk exposure, and capital adequacy. This transparency enables investors, analysts, and other stakeholders to better assess the potential risks associated with their investments. As a result, market participants can make more informed choices, fostering a more responsible and accountable financial environment.

Implications of the Capital Regulation Plan

The implementation of the CRP has had far-reaching effects on the finance industry and its various stakeholders. Some of these implications include:

Increased Stability

The anticipated increase in stability stemming from the Capital Regulation Plan is crucial for both financial institutions and the broader economy. By ensuring that banks maintain adequate capital levels, the risk of systemic failures is reduced. This creates a more resilient banking environment, where institutions can sustain operations during financial turbulence, thereby safeguarding consumer deposits and ensuring continued access to credit. Furthermore, the stabilisation of the banking sector encourages investment and economic growth, instilling greater confidence among businesses and consumers alike. As banks become more adept at managing risks and maintaining necessary capital buffers, the potential for future financial crises diminishes, leading to a healthier economic landscape.

Enhanced Consumer Trust

An often-overlooked implication of the Capital Regulation Plan is the enhancement of consumer trust in the financial system. With stronger regulations in place, consumers can feel more secure knowing that the institutions managing their funds are better equipped to handle solvency issues. This confidence can lead to increased participation in banking services, further stimulating growth within the financial sector. As consumers trust that their banks adhere to stringent capital requirements, they are more likely to engage in long-term financial planning and investments, ultimately contributing to a more stable overall economy.

Opportunities for Improvement

While the CRP has undoubtedly had a positive impact on the finance industry, there is always room for improvement. One area that regulators continue to address is the consistency of implementation across different regions and financial institutions. As Basel III is implemented differently by various countries, harmonizing these regulations can improve global financial stability. Additionally, ongoing research and analysis are crucial to identifying potential gaps in capital requirements and addressing emerging risks effectively.

Challenges and Benefits of the CRP

The Capital Regulation Plan has its fair share of challenges and benefits, some of which include:

Challenges

- Compliance Costs: The adoption and enforcement of CRP regulations can be costly for financial institutions, particularly smaller banks. These costs may trickle down to consumers through increased service fees or reduced interest rates on deposits.

- Uneven Implementation: As mentioned earlier, the uneven implementation of Basel III by different countries and regions can create discrepancies in capital requirements. This can result in a competitive disadvantage for certain banks while also posing potential risks to financial stability.

- Adapting to Changes: Financial institutions must adapt quickly to changes in regulatory requirements, including the introduction of new ratios or buffers. This can be challenging, particularly for smaller banks with limited resources.

Benefits

- Improved Stability: The primary benefit of the CRP is the enhanced stability of financial institutions and the overall banking system. By strengthening capital requirements and risk management practices, banks are better equipped to handle economic downturns or unexpected shocks.

- Greater Transparency: As discussed earlier, increased transparency in the banking sector benefits all stakeholders involved, from investors to consumers.

- Stronger Risk Management Frameworks: The CRP has prompted financial institutions to adopt more robust risk management frameworks, allowing them to identify and mitigate potential risks effectively. This ultimately leads to healthier financial portfolios and more informed decision-making.

Conclusion

In summary, the Capital Regulation Plan represents a significant evolution in the banking landscape, fostering a more resilient and transparent financial system. The emphasis on adequate capital reserves, rigorous risk management, enhanced transparency, and increased consumer trust culminates in a sturdy framework designed to withstand economic fluctuations. While challenges such as compliance costs and uneven implementation persist, the overarching benefits—improved stability, greater accountability, and a stronger foundation for risk management—underscore the necessity of such regulations in safeguarding the future of banking. As the financial sector continues to adapt to these changes, ongoing dialogue among regulators, institutions, and stakeholders will be essential to refining and advancing these standards, ensuring that they align with the ever-evolving market dynamics and global economic conditions.